Michael S. O'Brien is a principal in the Washington, DC office of Rusk O'Brien Gido + Partners. He specializes in corporate financial advisory services including business valuation, fairness and solvency opinions, mergers and acquisitions, internal ownership transition consulting, ESOPs, and strategic planning. Michael has consulted hundreds of architecture, engineering, environmental and construction companies across the U.S. and abroad.

Where Are A/E Valuations Heading?

Where Are A/E Valuations Heading?

October 19, 2022

With so much turmoil in the economy and stock market, many A/E business owners are probably wondering what this might mean for their own firm’s value. Interestingly, while the stock and debt markets are going through turmoil, many firms in the A/E industry, both publicly traded and privately held, continue making acquisitions, demonstrating revenue and backlog growth and seeking to hire more employees. Furthermore, the future pipeline of projects from federal, state, and local government agencies funded by the Infrastructure Investment and Jobs Act (IIJA), would generally signal rising future valuations for companies operating in the A/E industry. However, that may or may not be the case.

Equity markets are more heavily influenced by the debt market than any other leading indicator. The benchmark 20-year Treasury, from which the cost of capital is derived, has nearly doubled since the beginning of the year from 2.05% to 4.25% (as of October 13, 2022). At present, rising inflation rates are forcing the Federal Reserve to increase interest rates in an attempt to control inflation. This increases the cost of capital, which drives down equity valuations, all other things being equal.

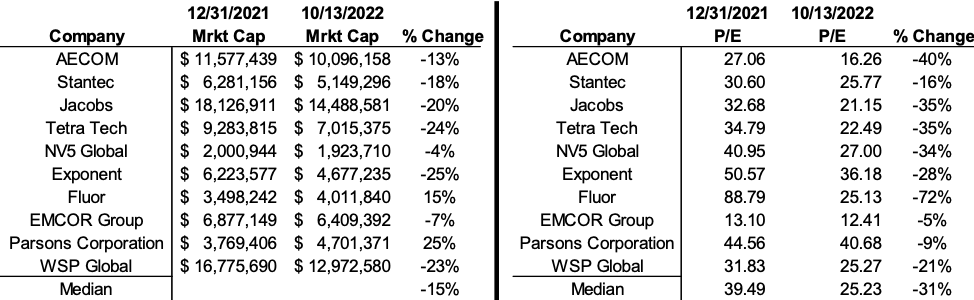

As of this writing, the major equity market indices — The Dow Jones Industrial Average, S&P 500, Nasdaq 100, and Russell 2000 (small cap index), are down 21%, 25%, 33%, and 26%, respectively. In addition to the decline in market capitalization, market multiples (P/E ratios) have also declined. The Schiller PE Ratio for the S&P 500 declined from 39.98x to 26.84x, or 30% since December 31, 2021. The mean and median Schiller PE Ratio since 1970 were 21.5x and 21.0x, which indicates that there is still more room for further decline. Comparing the market capitalization decline to the decline in PE ratios indicates that corporate earnings are up, but valuations are down. This analysis indicates that investors view the future as uncertain despite current earnings results.

As the chart below indicates, the median PE ratios of A/E firms are down 36%, much higher than the median decline in market capitalization. P/E multiples falling further than market capitalizations indicate that, as with the broader indices, earnings among the publicly traded A/E firms are up for the year.

Shiller PE ratio for the S&P 500. Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio)

While increasing earnings typically equates to an increase in stock value, this is not always the case. Of course, nothing is more disheartening than telling shareholders that while revenues are up and profits are up, the company's stock value is down. While it may seem counterintuitive, it’s an important reminder that value is driven by expected future cash flow. Investors across the broader stock market are selling equity investments because rising interest rates increase future cash flow risk.

Fortunately, with improving backlogs and stronger growth opportunities in 2023, firms in the A/E sector may be poised to outperform the larger economy, thanks in part to the aforementioned infrastructure spending. The prospect for continued industry growth in 2023 and beyond could very well offset the economic and market headwinds that are putting downward pressure on valuations at the end of this calendar year.

As a final note, firms that utilize formulas to determine their stock's value may want to examine those formulas to ensure that it does not stray too far from a reasonable value indication, particularly in light of the material changes in market conditions.

There’s still time to join us and nearly 200 A/E firm leaders in Naples, Florida, from November 2nd through November 4th at our annual Growth & Ownership Strategies Conference to hear from business & economic experts — and your industry peers in the market.

Mark Your Calendar!

Latest Perspective

Perfecting the A/E Exit Strategy – Five Key Factors

An enormous A/E generation that kicked off their careers in the 1980s and subsequently started firms or became owners in the 1990s ...

Studies

Latest Transactions

Financial Experts for Architects, Engineers, and Environmental Consulting Firms