Ian has spent the past twenty years working with hundreds of architecture, engineering and environmental consulting firms large and small throughout the U.S. and abroad with a focus on ownership planning, business valuation, ESOP advisory services, mergers & acquisitions, and strategic planning. Ian is a professionally trained and accredited business appraiser and holds the Accredited Senior Appraiser (ASA) designation with the American Society of Appraisers and is a certified merger & acquisition advisor (CM&AA) with the Alliance of Merger & Acquisition Advisors.

Inside The Latest A/E Business Valuation and M&A Transaction Study

February 7, 2023

With economic growth slowing and interest rates rising, it's not surprising that A/E firm valuation multiples have ebbed from their post-pandemic peaks. The latest valuation statistics from the recently released A/E Business Valuation and M&A Transactions Study (tenth edition) show that for all transaction types—minority interests in privately held companies, controlling interest (M&A) transactions, and public market transactions, valuations multiples have declined, albeit only slightly.

This year's survey included 241 transactions, including internal minority interest ownership transition transactions and controlling interest merger & acquisition transactions. The tables below illustrate the enterprise values of the surveyed firms as a multiple of earnings before interest and taxes (EBIT) and earnings before interest, taxes, depreciation, and amortization (EBITDA).

Minority Interest Enterprise Value Multiples

| Valuation Multiple | 2022 | 2021 |

|---|---|---|

| EV / EBIT | 4.78 x | 5.08 x |

| EV / EBITDA | 3.65 x | 3.83 x |

Controlling Interest Enterprise Value Multiples

| Valuation Multiple | 2022 | 2021 |

|---|---|---|

| EV / EBIT | 5.42 x | 5.76 x |

| EV / EBITDA | 5.34 x | 5.46 x |

With internal transactions, there are several factors at work. For many firms, valuations in 2021 were buoyed by excess liquidity resulting from forgiven Paycheck Protection Program loan proceeds. For firms establishing their value through independent valuations, higher rate of return expectations and lower market pricing of publicly traded A/E firm stocks are also factors in the lower valuations.

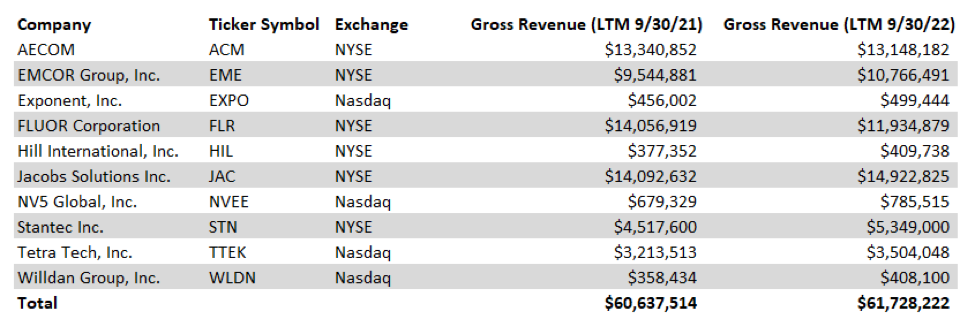

In addition to the data on privately held companies, the study tracked the growth and pricing of ten publicly traded A/E and environmental consulting firms over the past year. As the table shows, in aggregate, the gross revenue of the ten firms grew at a modest rate of 1.8% over the last year (using reported trailing twelve months' revenue through September 30th).

| Company | Ticker Symbol | Exchange | Gross Revenue (LTM 9/30/21) | Gross Revenue (LTM 9/30/2022) |

|---|---|---|---|---|

| AECOM | ACM | NYSE | $13,340,852 | $13,148,182 |

| EMCOR Group, Inc | EME | NYSE | $9,544,881 | $10,766,491 |

| Exponent, Inc. | EXPO | Nasdaq | $456,002 | $499,444 |

| FLUOR Corporation | FLR | NYSE | $14,092,632 | $11,934,879 |

| Hill International, Inc. | HIL | NYSE | $377,352 | $409,738 |

| Jacobs Solutions, Inc. | JAC | NYSE | $14,092,632 | $14,922,825 |

| NV5 Global, Inc. | NVEE | Nasdaq | $679,329 | $785,515 |

| Stantec Inc. | STN | NYSE | $4,517,600 | $5,349,000 |

| Tetra Tech, Inc. | TTEK | Nasdaq | $3,213,513 | $3,504,048 |

| Willdan Group, Inc. | WLDN | Nasdaq | $358,434 | $408,100 |

| Total | $60,637,514 | $61,728,222 |

Amounts in Thousands

In spite of this modest growth, or perhaps because of it, the total value of this portfolio of publicly traded firms, as measured by aggregate market capitalization, declined 4.6% over the same period. Interestingly, this decline in market capitalization correlates closely to the observed decline in private company valuation multiples.

About the Study

The 10th edition of the A/E Business Valuation and M&A Transaction Study is available online at www.rog-partners.com/aestudy. The study is designed to inform industry executives of current trends in the transacted values of architecture, engineering, and environmental consulting firms. This study is different from others because it is based on actual transactions instead of reported valuations. These include transactions by and between employee-owners, employee stock ownership plan (ESOP) transactions, and mergers/acquisitions. The study includes data on ten separate valuation multiples and 23 financial performance metrics. Multiples are separately reported on a controlling interest, minority interest, and ESOP ownership basis.